Sanghvi Movers is a case for potential business turn-around after its revenues fell by half in FY2018 and profits reduced from Rs 109 Crs in 2017 to a loss of Rs (-57) Crs in FY2018

There are specific reasons for this dramatic fall in business fortunes and there are hints of light at the end of the tunnel. This could turn out to be an interesting opportunity. Let us delve a little deeper.

- Sanghvi Movers – The Business Case

Sanghvi Movers is in the business of supplying cranes on rental basis for erection and commissioning of infrastructure projects (port infra, wind mills, thermal power plants, metro projects, refineries etc).

Sanghvi Movers is the largest crane leasing company in India and the 6th largest in the world.

Approximately 80% of its business comes from installation of wind mills and thermal power plants.

- What went wrong for Sanghvi Movers – History of capacity addition in Wind Energy Sector

Before FY18, the wind and solar energy projects used to work on cost-plus tariff mechanism. This meant the government (state/central) framed rules in such a way that solar/wind projects were guaranteed to make profits. This meant the pace of capacity addition of wind energy projects was brisk.

In FY2018, the government changed the rules of the game for renewable energy (Wind and Solar). Instead of cost-plus tariffs, the government decided to go ahead with competitive bidding.

Capacity installations dramatically dropped in FY18

- Fundamental cost economics have changed

- After the switch to competitive bidding, the tariffs discovered for wind energy came down from around Rs 5.5 per unit to around Rs 2.5 per unit.

- As per the CERC, the average power purchase cost at all-India level is Rs 3.53 per unit.

- Thus, wind energy has today become the cheapest source of power in India.

- This means that not only do wind energy projects not require any government subsidies/cost incentives, but wind energy has become the most desirable source of energy for the buyer; as it is also the cheapest source of energy.

- Simply put – wind energy is in more demand than the largest source of energy in India – thermal power produced from coal.

- Wind Energy Potential of India

- The National Institute of Wind Energy estimates the wind energy potential1 of India to be approximately 3,00,000 MW.

- Total installed wind capacity as on 31.03.2018 is 34,046 MW.

- This means at least for the next 5-10 years, there is enough scope and ready potential available to expand wind energy capacity.

- With wind energy becoming the cheapest source of power, competitive forces have taken over and the pace of capacity addition is expected to dramatically increase in the next few years.

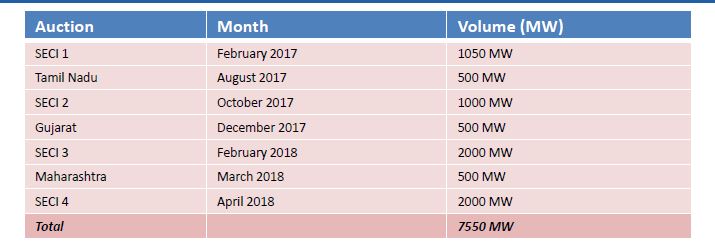

- Competition at Play – Wind Project Auctions in the last 15 months

Solar Energy Corporation of India (SECI) – the agency designated by Indian Government to help implement the renewable program of the government has come out with several auctions in the last 15 months for wind energy projects. Total of 7550 MW of wind energy projects have been bid out in the last 15 months.

This means the pace of capacity addition in the wind energy sector will gather momentum in the near future on the back of Power Purchase Agreements signed with SECI.

After the Letter of Award (LOA), a wind energy project typically requires about 18-24 months till completion (commissioning). Thus, the project execution contracts of the above 7550 MW worth of projects will reflect in the revenues of Sanghvi Movers in FY19 and FY20.

- Impediments to Project Implementation

- The wind energy project needs to be connected to the transmission network – inter-state transmission network typically implemented by Powergrid

- Connectivity with the Grid (transmission network) is a major constraint. Many wind energy developers had taken connectivity (without financial commitments) even before they have won the bid in any tariff based competitive bidding regimes.

- This meant that Powergrid (transmission utility) does not have the capacity to grant connectivity to the winners in the SECI/State auctions.

- This has delayed the issuance of Letter of Award (LOA) in some cases and has also resulted in the cancellation of some of the future auctions of new projects in pipeline.

Eg. Auction of 2000 MW of wind projects under SECI Tranche V was cancelled in May-18 due to poor bidder response on account of missing clarity on transmission access.

- Also a wind project is implemented in 18-24 months, while building a new inter-state transmission network takes a minimum of 48 months. This could lead to mismatch in the project implementation timelines of generating stations and transmission infrastructure

- However, after a long-drawn out process of regulatory consultation and deliberation which lasted almost a year, Central Electricity Regulatory Commission (CERC) has come out with amendments to the existing regulations that have tried to solve the above problems of entities successful in the above SECI/state government auctions. The regulatory uncertainty has been cleared.

- Why Sanghvi Movers and not a wind energy generator/EPC player (Eg Inox Wind/Suzlon)?

- Sanghvi Movers is a asset-heavy business model and a single business segment – leasing of cranes.

Sanghvi Movers is the largest crane leasing company in India.

Installation of wind mills requires cranes and any increase in wind energy capacity addition will have a direct impact on the revenues (EBIDTA) of Sanghvi Movers. - Also, the business of Sanghvi Movers was more than halved in FY18 due to slowdown in wind energy capacity additions and thus, revival in wind energy capacity addition will have a very visible and immediate impact on the financials of Sanghvi Movers.

- Though a similar directional effect is also expected on the financials of EPC players in wind sector and wind energy generators, we need not take on additional risks of project execution, land acquisition and other approvals and transmission network availability risks by investing in those companies

- Q1FY19 Update

The quarter results have come out on 13.08.2018 and its not happy news.

Though 7550 MW of wind power projects have been auctioned from Feb-17 till Jul-18, the capacity addition is now expected to be around 3000 MW instead of the better case scenario of 4000-5000 MW.

This is due to the reasons already discussed above – unavailability of sufficient transmission network, non-signing of PPAs (Power Purchase Agreements) by the respective Distribution Companies (DISCOMs).

Thus, though there are clear signs of revival in capacity addition, the path to execution is not simple.

- What can go wrong with the investment thesis?

There are three major risks to the above investment thesis

(a) Since capacity utilization of Sanghvi Movers has dropped to below 40% for the last 9-12 months, when the demand for cranes comes, they will be leased out at lesser rentals. Thus, operating profit margins may take a hit.(b) Large write-offs of old receivables.

Receivables stand at Rs 134 Crs which is almost 60% of FY18 revenues(c) Issues with transmission network availability (discussed in detail above) impact the pace of wind projects capacity addition - Valuations – Sanghvi Movers

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| Sales (Rs Crs) | 332 | 361 | 450 | 339 | 244 | 308 | 531 | 553 | 228 |

| Operating Profits (Rs Crs) | 253 | 256 | 317 | 232 | 136 | 179 | 347 | 366 | 84 |

| Operating Profits (%) | 76% | 71% | 70% | 68% | 56% | 58% | 65% | 66% | 37% |

| Total Debt (Rs Crs) | 474 | 639 | 700 | 592 | 465 | 334 | 602 | 538 | 520* |

| Enterprise Value (Rs Cr) | 1,446 | 1,167 | 1,168 | 907 | 790 | 1,605 | 1,861 | 1,597 | 1,232 |

| EV/EBIT | 8 | 7 | 5 | 7 | 34 | 24 | 8 | 7 | N/A |

*As on 30.06.2018

- Given the capital intensive nature of the business and the fact that the business of Sanghvi Movers is highly cyclical and dependent on performance of core infrastructure sector, I am willing to pay a EV/EBIT multiple of not more than 7. (double the Triple AAA bond yield)

- It may be reasonably estimated that approx 3000 MW of wind energy projects may get installed in FY19 and thus revenues of Sanghvi Movers may move upto around 400-450 Crs. More installations will happen in FY20 and sales may further improve.Thus, EBIT of Sanghvi Movers is likely to increase from Rs (-53) Crs to about Rs 200 Crs in FY19

- Thus at EV/EBIT of 7, the EV comes to around Rs 1400 Crs.

- Considering a 20% discount to our valuation as a margin of safety, Sanghvi Movers is a buy when the Enterprise Value (EV) reached Rs 1100 Crs ie at a price of Rs 135 per share.

Further analysis required to develop more conviction in the idea

- Winners of each of the SECI auctions and the tariff discovered

- Connectivity and Long Term Access status of each of the winning bidders

- Project progress of constructing transmission infrastructure by Powergrid

- Penalties for not completing the project or abandoning it midway

References

- Potential of Wind Energy – Data from National Institute of Wind Energy

http://niwe.res.in/department_wra_100m%20agl.php

- Q1FY19 Investor Presentation – Inox Winds

- Q1FY19 Investor Presentation – Suzlon

- Q1FY19 Investor Presentation – Sanghvi Movers

- Annual Reports of Sanghvi Movers over the years

- Solar Energy Corporation of India

http://seci.co.in/ - Average Power Purchase Cost (All-India) = Rs 3.53 per unit http://www.cercind.gov.in/2018/orders/FinalOrder.pdf

- PPA signed for Tranche I (SECI Wind Power Auctions)http://pib.nic.in/newsite/PrintRelease.aspx?relid=168838

- Wind power auction of 500 MW in Tamil Naduhttps://www.business-standard.com/article/companies/wind-power-tariff-tumbles-further-to-rs-3-42-per-unit-in-second-auction-117083000458_1.htmlTotal of 900 MW of projects awarded. Project to be completed within 10 months of signing the PPA

Disclaimer – The analysis presented above is just for study purposes to illustrate the process of analyzing businesses and stock investment opportunities. The article may not be construed as a recommendation to either buy/sell the stock of the concerned company

I am a SEBI registered Investment Advisor.

4 Responses

“However, after a long-drawn out process of regulatory consultation and deliberation which lasted almost a year, Central Electricity Regulatory Commission (CERC) has come out with amendments to the existing regulations that have tried to solve the above problems of entities successful in the above SECI/state government auctions. The regulatory uncertainty has been cleared”

can you please provide link that justify above statement?

Thanks

Prashant

Hi Prashant

Here is the link to the CERC Order with regards to Connectivity and Long Term Access to Renewable Energy Projects

http://www.cercind.gov.in/2017/orders/145_MP.pdf

This order led to a consultation process that changed the Procedure for Grant of Connectivity and Long Term Access

http://www.cercind.gov.in/2018/regulation/139_ANX.pdf

These are enabling provisions and mean that the deficiencies in regulations which were affecting renewable energy project additions have been removed.

The actual physical availability of transmission network and access will slowly follow suit.

What is a current update on wind mill installations, if you have any idea can you please update?

Thank you

Hi Prashant

189 MW of capacity was added in Apr-19

One may compare the monthly reports for installed capacity at the CEA website to arrive at these figures

http://www.cea.nic.in/reports/monthly/installedcapacity/2019/installed_capacity-05.pdf

At the same time, the transmission capacity constraint at Bhuj in Gujarat is a thing of the past.

Installation of the Transmission Sub-station at Bhuj is complete as per the Mar-19 CEA transmission status reports.

(Check out the latest Con Call Q4FY19 of Inox Wind – the management also confirms this)

4000 MW of SECI auctioned wind projects are coming up at Bhuj alone.

Now what remains is installation of transformation capacity which is in progress and expected to be progressively delivered over the next 14-16 months.

http://www.cea.nic.in/reports/monthly/transmission/2019/monthly_trans_inter-04.pdf

My estimation is that the entire 4000 MW of wind projects at Bhuj will be commissioned before Oct-20