Would you like to invest in a company whose operating profits have gone up 12 times from just 9 Crs to 107 Crs in the last 18 months and is still trading at a PE ratio of just 10?

On top of that the company is expanding capacity in 2 of its major products by more than 50% in the next 12 months?

The original article was published in the Moneylife Magazine on 03.01.2019

https://goo.gl/SdkH2r

What follows is a slightly modified version of the original Moneylife article.

We are talking about a four decades old chemical company having its manufacturing facilities at Roha, Raigad district in Maharashtra.

The company – Sadhana Nitro Chem manufactures nitrobenzene derivatives mainly – Meta Amino Phenol (an intermediate), metanilic acid (an intermediate) and ODB2 (a colour former commonly used in thermal paper industry).

The products of the company are used as chemical intermediates and find application in end-use industries like apparel, paper, hair dyes, pharmaceuticals, cosmetics, agro chemicals, aerospace and military applications (attire).

Have a look at the stock price chart over the last 3 years

The stock has gone up 30 times in less than 3 years.

The stock has gone up 30 times in less than 3 years.

Let us analyze the numbers behind this phenomenal increase in stock price.

| Sadhana Nitro Chem | Mar-16 | Sep-18 |

| Revenue (Rs Crs) | 35 | 229 |

| PAT (Rs Crs) | -5 | 81 |

| Total Debt (Rs Crs) | 33 | 3 |

| Debt/Equity Ratio | 13 | 0.3 |

| Receivables Days | 107 | 34 |

| Inventory Turnover | 3.8 | 6.3 |

| Fixed Assets (Net) | 29 | 52 |

What is the reason for the dramatic turnaround in the fortunes of this company?

In fact, Sadhana Nitro Chem made losses in 6 out of the last 10 years.

If we dig a little deeper, and find out the prices of the end-product that the company manufactures, this is what we uncover.

Price Chart – 3 year historical export prices for Metanilic Acid

The market price of Metanilic Acid has gone up by almost 2.5 times from around 150 Rs/Kg to around 350 Rs/Kg in the last 1 year.

Price Chart – 3 year historical export prices for Meta Amino Phenol Acid

The market price of Meta Amino Phenol has gone up by almost 2.5 times from around 550 Rs/Kg to around 1700 Rs/Kg in the last 1 year.

The market price of Meta Amino Phenol has gone up by almost 2.5 times from around 550 Rs/Kg to around 1700 Rs/Kg in the last 1 year.

The main input raw material for making these end-products is benzene (C6H6) which is widely and easily available and whose prices have not gone up significantly in the last 1 year

Price Chart – 1 year historical export prices for Benzene

The market price of Benzene has gone up by only about 25% from 48 Rs/Kg to 61 Rs/Kg.

The market price of Benzene has gone up by only about 25% from 48 Rs/Kg to 61 Rs/Kg.

Thus output product prices have gone up multiple times in the last 1 year, whereas input product price has not gone up much.

If we analyse the last 10 years Profit & Loss statement of the company, we realize that raw material cost (benzene, nitric acid, caustic potash, sulphur based chemicals, iron ) has been around 60%.

In fact as of the Sep-18 quarter, the raw material costs have fallen to just 25% of the revenues.

This 2.5 times increase in end-product prices along with only a slight increase in input raw material prices has resulted in the dramatic increase in the profits of the company in the last 18 months.

So this completes our quick analysis of what the company does, how have the financial numbers changes over the last few years and why has the stock price gone up 10 times just the last 1 year.

Let us now make an assessment of management pedigree.

On 18th May-18, CRISIL came out with a modification to the credit rating of Sadhana Nitro Chem.

CRISIL mentioned that the company has not been co-operating with the rating agency and has not been providing adequate data to CRISIL. This was despite several follow-ups through official letters and telephonic calls.

This definitely does not augur well for the way in which Sadhana Nitro Chem is conducting its affairs.

However, with hindsight and the fact that the company has almost paid back its entire debt as of 30-Sep-18, the company probably did not have any need of a credit rating.

The credit rating report also mentions that Sadhana Nitro Chem has not even paid the rating fees to CRISIL. In all probability the management knew that with end-product prices increasing in such a short span of time, the company will be able to pay down all its debt and thus may not need a credit rating report which is typically used by bankers and institutions to assess credit worthiness.

Non-cooperation with the credit rating agency is a big red flag and typically points to accounting fraud. However, if the management wanted to save a few lacs of credit rating agency’s fees and hence did not cooperate, it is an important insight into how the management conducts its affairs.

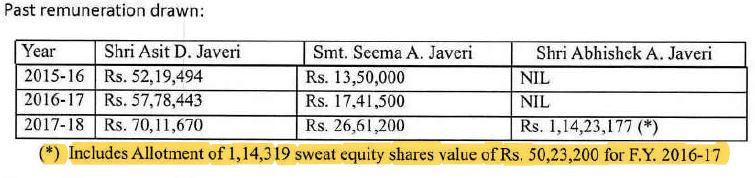

One of the easiest ways of assessing management intentions and treatment of minority shareholders is to check the remuneration over the past several years especially the change in remuneration wrt to change in profits/revenues.

| Salary | Asit Javeri (Chairman) | Seema Javeri (Spouse) | Abhishek Javeri (Son) | Total |

PAT |

| 2015-16 | 52 Lacs | 13 Lacs | NIL | 65 Lacs | -5 Crs |

| 2016-17 | 58 Lacs | 17 Lacs | NIL | 75Lacs | 1 Crs |

| 2017-18 | 70 Lacs | 27 Lacs | 64 Lacs | 161 Lacs | 31 Crs |

| 2018-19 | 168 Lacs | 168 Lacs | 168 Lacs | 504 Lacs | 81 Crs |

Though the company has made substantial progress and has turned extremely profitable from being loss making in Mar-16, the rise in management remuneration is very steep.

The increase in the Chairman’s salary who is spearheading the company for 40+ years is very well justified.

However same level of salary to the CFO (son of the Chairman) who has joined full-time just 2 years back and same level of salary to the Executive Director – Administration (wife of the Chairman) is definitely a red flag, especially given the fact that the management seems to have very little hand in the company turning profitable.

As analyzed earlier, the end-product prices have risen by more than 2.5 times and that is the sole reason for the company turning profitable. The market prices for the end-product are not in control of the company and the prices may reduce in the future and just as Sadhana Nitro Chem made losses in the last 6 out of 10 years, the company may actually become unprofitable sometime in the future.

There is solace in the fact that the company has liberally increased the remuneration for the workers (28%) and the management cadre (24%) in year 2017-18. But compared with more than 100% increase promoter family remuneration in 2017-18 and further more than 300% increase in 2018-19, salary increases for the staff are meager.

Compare this with the salary of DGM (Production) Mr G K Kutty employed with the company since 1979 which is only Rs 10 Lacs.

Now let us analyze the case preference shares allotted to the promoters.

17.5 Lac preference shares (9% cumulative non-convertible preference shares of face value Rs 10) were allotted in the year 2012-13 and a further 78.5 Lac preference shares (9% cumulative non-convertible preference shares of face value Rs 10) were allotted to the promoters in the year 2015-16.

Since the company was loss making in the intervening years, the interest on the cumulative preference shares was supposed to be paid in the years that the company made profits.

The total interest outgo over the last 6 years would be approximately Rs 2 Crs in total.

Thus, in case the preference shares were redeemed at par sometime in 2018-19, the total outgo for the company would be Rs 9.6 Crs (principal) + Rs 2 Crs (cumulative interest).

Now let us see how the events unfolded.

The company in the year 2017-18 modified the terms and conditions of the preference shares from 9% cumulative nonconvertible to 1% non-cumulative non-convertible preference shares.

In fact the cumulative interest that was due till 31.03.2017 was also waived off.

At the face of it, this modification of the terms looks favourable to the company. However, the redemption terms were changed from to be redeemed at par to redemption at a 80% premium after the company turns profitable.

Thus, with the change in the terms and conditions, the total outgo in case the company makes enough profits was changed to Rs 17.3 Crs instead of approx Rs 12 Crs.

The company did turn profitable, and redeem the preference shares at a premium and paid the promoters Rs 17.3 Crs in Jun-18.

Now the promoters have a privileged view of the business over the minority shareholders. The products of the company are commodities and price fluctuations (increase/decrease) are common across all commodities across the world. The significant increase in the end-product prices was seen by the promoters before it became common knowledge in the general minority shareholder population.

Thus, the sequence of events surrounding the modification of terms and conditions of the preference shares and their subsequent redemption at a significant premium does caste doubts on the shareholder friendliness of the mangement.

The Rs 5.3 Crs extra benefits that the promoter entity enjoyed may not seem very high especially in relation to the trailing 12 months profits of Rs 81 Crs, however the manner in which the management has conducted itself casts doubts on their willingness to share the fruits of the business with the minority shareholders.

Allotment of sweat equity

Good management can make a huge difference to the fortunes of the business and consequently to the share price of the stock over the long-term. Competent and superior management must be rewarded through monetary and other non-monetary benefits.

On 28-Mar-2018, the company allotted 1,14,319 sweat equity shares to the CFO ie a 1.2% stake in the company.

When the annual report came out, it became clear that the price considered for allotment of sweat equity was around Rs 44 per share and the entire 1.14 Lac sweat equity shares were values at Rs 50.23 lacs.

The day on which this allotment of 1.2% sweat equity stake was made, the stock price was already Rs 219 per share and within the next 9 months, the stock price increased to Rs 930 per share.

The 1.2% sweat equity stake in now worth approx Rs 11 Crs.

Now this may seem purely coincidental to anyone, however one has to look at the overall picture. The CFO had joined the full-time services of the company on 01-Apr-2016, just 2 years back.

The profit of the company for the previous 4 quarters prior to the allotment of sweat equity was

The profit for the next 3 quarters

Did the management have a premonition that certain market developments will cause the company to become massively profitable and make bumper profits that the company has not made in the last 10 years combined?

As discussed in the earlier part of the article, the end-product prices had started increasing in Dec-17 itself and the company over the next 12 months made significant profits.

When the sweat equity of 1.2% of the company was allotted to the CFO, the management had a premonition that Sadhana Nitro Chem is likely to make huge profits in the next few quarters and consequently the stock prices are also expected to increase substantially.

The allotment of the sweat equity on 28-Mar-2018 valued at just Rs 0.52 Crs proved to be a windfall gain of Rs 11 Crs. To the credit of the promoters, none of them have sold any of their shares in the last 1 year.

After analyzing the company in depth and also looking at the management pedigree, let us now come to the question we asked ourselves in the beginning.

Should I invest in this company?

The end-product prices have jumped significantly over the last 1 year and the company today is very profitable and also available at a PE ration of just 10.

Given the history of losses in the company and the doubtful pedigree of the management, the only reason why one might invest in this stock is if one has strong reasons to believe that the end-product prices will stay high or climb higher for a long time in the future.

Now, what is the reason that the end-product prices of the company have risen?

Let us hear it from the management itself.

As can be confirmed from several other sources and what the management itself says in the Sadhana Nitro Chem annual report for 2018, the major reason behind the sudden jump in end-product prices is because of pollution control measures in China.

China constitutes about 40% of the global chemical industry. The country in known for massive manufacturing capabilities and technology in several industries including steel, textiles, chemicals, mining, metals, power, aerospace, automobiles and a number of others.

Though China has started implementing its environmental measures strictly over the last 2-3 years, China is capable of shifting its industries from populated cities to far off provinces in a reasonably short time period and restart production with larger capacities.

Given that the end-products of Sadhana Nitro Chem are fairly common chemical intermediaries, in my opinion the product prices will not remain so high for too long.

If one has some special knowledge/insights in the end-product prices of Meta Amino Phenol (an intermediate), metanilic acid (an intermediate) and ODB2 and can come to know of the trend for product prices before it becomes common knowledge in the investor community, one may think of buying this stock at the current price levels (Rs 930 per share).

In either case and especially in light of the management assessment above, one is better off giving this opportunity a pass.

6 Responses

Hello,

From where did you got the historical prices of chemicals mentioned above??? Can you please share the link???

Hi Yash

The historical prices are available at

https://www.screener.in/hs/

However, you would need to subscribe for the gold membership of Screener.

Very good Informative

Good one, Amey!

Though read little late but a good read.

The articles are precise and very informative. Just want to know about chemical company which is sound for future investment. The problems in China can benefit this sector in India for next few years.

It’s truly informative.

Thanks for sharing.