The stock price of Piramal Enterprises has cracked in the last 2 weeks. The name of Piramal Enterprises is now taken in the same breath as that of DHFL, Reliance Capital, Yes Bank, Indiabulls Housing Finance and other wealth destroyers.

If you are an investor in Piramal Enterprises, what should you do with your holding?

And even if you are not a Piramal shareholder, this article could provide an interesting perspective on investing and business valuations.

Let us directly jump into the valuations and get our hands dirty

Sum of Parts Valuation of Piramal Enterprises

Piramal Enterprises comprises of four parts

- Pharma Division

- Healthcare Analytics and Insights Division

- Stake in Shriram Group

- Lending business

Valuation of the Pharma Business

Let us look at the valuation at which the peers of Piramal Enterprises (pharma business) trade at

| Valuation | Torrent Pharma | Cipla | Dr Reddy’s | Lupin | Sun Pharma | Divis Lab | Biocon |

| EV/EBIT* | 24 | 20 | 24 | 21 | 21 | 26 | 28 |

* EV = Enterprise Value

* EBIT = Earnings Before Interest and Tax

Piramal’s pharma business comprises of complex branded generics and contract manufacturing for global pharma companies. All the manufacturing plants are based out of Europe. We can safely assume that Piramal should trade at similar valuations ie an EV/EBIT =22

For Piramal (Pharma division)

EBIDTA (2019) = Rs 1100 Cr

Depreciation = Rs 380 Cr

Thus, EBIT = Rs 720 Cr

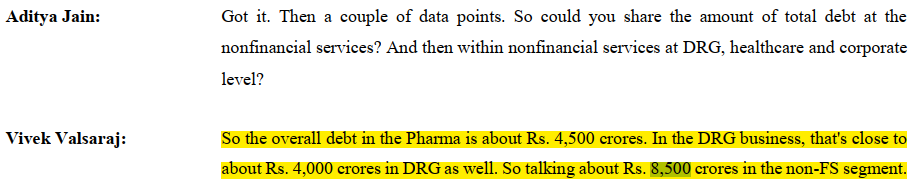

Debt attributable to the pharma business are approximately Rs 4,500 Cr. We get this data from the conference call of Q4FY19

Debt in pharma business = Rs 4,500

Reverse calculated EV = 720*22 = Rs 15,800 Cr

Thus, we can assume that if the pharma business gets separately listed, the market will give a valuation of

Piramal (pharma division) market-cap = Rs 11,300 Cr

Stake held in Shriram Group

As of 31.03.2019, Piramal Enterprises held

- 20% stake on Shriram Capital (unlisted)

- 10% stake in Shriram Transport Finance (22.6 Mn shares)

- 10% stake in Shriram City Union (6.58 Mn shares)

Let us calculate the value of the Shriram stake held by Piramal Enterprises as of today

- Shriram Capital (unlisted) = Rs 2,150 Cr (at cost)

- Shriram Transport Finance = Rs 2,300 Cr (stake sold in Jun-19)

- Shriram City Union = Rs 850 Cr (at a share price of Rs 1325 per share)

Total stake in Shriram Group is worth about Rs 5,500 Cr.

Valuation of Healthcare and Analytics Division

Total Equity invested in healthcare analytics = Rs 1,300 Cr

(Estimated from the segment results and the fact that Rs 4,000 Cr debt is attributable to the DRG business)

Revenue for 2019 = Rs 1,330 Cr

This division is not performing too well and is probably loss-making.

Let us make a guess that if Piramal decided to sell this business tomorrow, Piramal will be able to recover around 50% of the equity invested in the business (this is just a wild guess)

Valuation of Healthcare business = Rs 700 Cr

Valuation of Lending business

Total Equity in lending business is Rs 12,000 Cr

Clearly, the trouble is in the lending business of Piramal Enterprises and the stock price has crashed because of the doubts surrounding the real estate loan book.

Stock price as on 10th Oct-19 = Rs 1358

Market Cap = Rs 27,010

Sum of parts valuation of Piramal Enterprises

- Pharma Division = Rs 11,300 Cr

- Healthcare & Analytics = Rs 700 Cr

- Shriram Stake = Rs 5,500 Cr

Total of 3 divisions = Rs 17,500 Cr

Thus, the market is giving the lending business of Piramal Enterprises a valuation of

27,010 – 17,500 = Rs 9,500 Cr

This comes to P/B value of 9500/12000 = 0.8 times P/B

Let us look at which of the lending businesses are trading at such a cheap valuation

| Lending Business | Yes Bank | Band of Baroda | SBI | PNB | South Indian | Bank of India | Allahbad Bank |

| P/B value | 0.4 | 0.7 | 1 | 0.6 | 0.35 | 0.5 | 1.1 |

| Gross NPA | 5% | 10% | 7.5% | 17% | 5% | 15% | 17% |

Thus, the market is valuing the lending business of Piramal Enterprises on par with public sector banks with gross NPA ratios of anywhere between 10% to 17%.

On the other hand, some of the well-managed private NBFCs and banks are trading at between 2 to 5 times book value eg HDFC Bank, Cholamandalam, Muthoot Finance, Manappuram Finance, AU Small Finance Bank etc.

So, it all boils down to how much trouble is the lending business of Piramal Enterprises is in?

It is widely known that liquidity in the market for NBFCs especially those who have an exposure to residential real estate developers has dried-up after the IL&FS default in Sep-18.

- Real estate has been stagnating since the year 2014.

- Inflation has been low – around 3% since 2014.

- Real Interest rates have been very high for a long-time now.

- Demonetization and implementation of RERA have considerably slackened the demand for real estate and the recent slowdown in the economy has dealt a mortal blow to many real estate developers and NBFC businesses.

Consequently, companies like DHFL, Reliance Home Finance, Altico Capital have defaulted on loans and several others are on the verge of collapse.

Even though Piramal would have taken enough security and cash cover from all the entities that it has lent to, the company can still go bankrupt once the lenders to Piramal pull out their money. This is exactly what happened with DHFL and Altico Capital. The gross NPA ratios of both the NBFC companies were well within control, but the banks that have lent to these NBFCs lost confidence in them and thus stopped lending to them. This resulted in asset-liability mismatch and both the companies went bankrupt.

Will Piramal Enterprises also go bankrupt?

One can only make an educated guess based on the data we have from various public sources like credit rating reports, annual reports, quarterly presentation, con call transcripts.

Let us look at some hard data. One very good source to read about a NBFC business is the credit rating reports.

Credit Rating report of Altico Capital (before default)

https://www.indiaratings.co.in/PressRelease?pressReleaseID=38482&title=India-Ratings-Downgrades-Altico-Capital-India-to-%E2%80%98IND-A%2B%E2%80%99%3B-Outlook-Negative

- 31% of the loan book is to real estate projects at the approval-stage (construction has not started)

- 70% of the loan book is under moratorium as on Jun-19 ie the borrowers have to only pay interest and principal repayment has not yet started.

Given that such a large part of the loan book was to approval-stage projects and most of the loans were in moratorium, the banks lost their faith in the ability of Altico Capital to recover their loans in time. Thus, the banks stopped lending additional funds to Altico and the company collapsed.

Credit Rating report of KKR India Financial Services

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/KKR_India_Financial_Services_Limited_October_01_2019_RR.html

- 70% of the loan book is under moratorium

- Though gross NPAs are 2%, they are expected to substantially increase in the next few months

Credit Rating report of ECL Finance (Edelweiss group)

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/ECL_Finance_Limited_October_04_2019_RR.html

- A “sizeable portion” of the wholesale book is currently under moratorium with bullet/staggered repayments

- Asset quality in the past has been supported by “active refinance market” especially for real estate.

What is the position of Piramal Enterprises?

Compared to the other troubled NBFCs, about 35% of the lending book of Piramal Enterprises is under moratorium – not a small number, but not too big either.

What does the credit rating report for Piramal tell us about its ability to resolve cases of stressed assets?

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Master%20Trust%202019%20Series%20I_September_27_2019_RR201909270606.html

Piramal Enterprises has demonstrated its ability to resolve loan cases with stress in one of the following ways

Piramal Enterprises has demonstrated its ability to resolve loan cases with stress in one of the following ways

- Bring in a strong developer to take over the project and the loan.

- Initiate legal action to monetize additional security already provided by the borrower.

- Providing extra loans so as to ensure completion of projects – comprehensive workaround.

Thus, losses from defaulting or stressed assets have been minimal so far.

Is there a silver lining?

There is – though real estate sales have been very sluggish for the last several years, those projects which the customer is sure of getting completed are selling well. There are two reasons why projects don’t get completed on time

- Cash shortfall for the builder

Piramal is typically the only lender to the real estate developer and if it makes sure that the project gets completed, the real estate will be able to sell and repay the loans to Piramal.

- Commercial real estate in doing very well – 23% of the Piramal loan book is for commercial real estate

Reading the quarterly presentation, con call transcripts and other documents, we realize that out of the total loan book of about Rs 56,000 Cr,

- only 48% is towards residential real estate.

- 90% of the residential real estate loan book is towards construction finance and

- 66% of the book is for late-stage projects – which are nearing completion.

Though the Indian economy is in a slow-down and the real estate is sluggish, the situation is far from desperate. Real estate has seen far worse days in 2009 and back in 1997 during the Asian currency crisis. (Check out this link about property price crash in 1997). If the construction of the real estate project is not hampered, the real estate developer is and will be able to sell the inventory at a reasonable price and repay the Piramal loans.

The latest press release on 10th Oct-19 does have some interesting data points to ponder upon.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/23c83562-8f57-45f4-8dad-7bac12111361.pdf

Piramal Enterprises has raised Rs 24,000 Crs of long-term loans from financial institutions in the last 1 year. All the lenders would have definitely done a rigorous due diligence on the underlying assets of Piramal with far more data than what we have access to.

Piramal has issued a pass-through certificate (PTC) in Sep-19. The structure of this PTC is very interesting and unique and is the subject of a separate article. The fact that there is demand for the PTC of Piramal Enterprises goes to show that the counter-parties are not dis-comfortable with the asset quality of the underlying loans.

Piramal Enterprises has been able to borrow additional Rs 3,000 Cr from public sector banks in Sep-19 which was one of the worst periods for raising additional debt capital.

Gross NPAs are still below 1%, but this is a metric we will be watching very closely.

Gross NPAs are still below 1%, but this is a metric we will be watching very closely.

So, what should I do with my Piramal holding?

In my opinion, the stock market is pricing the Piramal Enterprises stock for bankruptcy of the lending business. It is not distinguishing between the credit underwriting skills of a company like Altico Capital, KKR India and Piramal Enterprises. Unlike a DHFL, Reliance Home Finance

This is not a time to sell the stock in distress at severely depressed prices. Just assume that you have gone on a vacation to the snowclad mountains of Lahaul and Spiti in Himachal Pradesh and return after 6 months to bother about the stock market and your investments in Piramal Enterprises.

What could prove me wrong?

- It is my assumption that the pharma and healthcare analytics are decent businesses with reasonably steady earnings predictability.

- There is an uncontrollable rapid rise in the NPAs and stressed assets at Piramal Enterprises.

- Piramal is not able to raise long-term debt funds in time from banks and institutions.

Is the price low enough for me to buy into the stock?

A lending business depends on the mercy of strangers (banks in case of Piramal) lending it money especially during crisis periods like what we are witnessing now. The business model is inherently risky. Though I am of the opinion that one need not sell their current holding in Piramal right now, I do not advocate buying into the Piramal stock at this price.

The problems and risks faced by Piramal Enterprises are largely out of the control of the management and we never know what will be the worse-case scenario. The intelligent investor is better-off trying to find some quality bargain businesses elsewhere. If one searched hard enough, one can find some good investment opportunities in this bear market.

One such example is

https://candorinvesting.com/2019/09/04/stocks-for-the-bear-market-cyclical-play-ashok-leyland/

Disclaimer:

Please do not consider this article as a stock recommendation. The article is an illustration of the kind of analysis that goes into fundamental research and equity investing. I continue to hold shares in Piramal Enterprises.

Please seek advice from your investment advisor before making any investment decisions.

The author (@amey153) is a SEBI registered Investment Advisor.

If you want to seek investment advice click here and someone from my team will get in touch with you within 48 hours.

11 Responses

Very well researched article. Kudos to you.

Good Article, learnt a lot.

Well researched

Good analysis. Can we have a similar one for Edelweiss please?

How have you included STFC in your valuations. They have disposed of this asset. And wholesale book cannot be valued on peer comparison basis.You have to go asset by asset to have a fair idea of what the asset is ?

We as retail investors do not have the data to make an asset by asset valuation.

We have to take a decision on whatever information we have.

The reason I have still included the STFC stake separately is because if you check the Q3FY19, Q4FY19, Q1FY20 presentations, they don’t seem to have allocated this capital to the lending business yet and probably still show it as “unallocable corporate assets”.

The article gives a framework to think about this stock. If you agree with the valuation methodology, feel free to make suitable adjustments as you feel appropriate

Stake held in Shriram Group is worth Rs. 5500 crores out of which stake valuation of Shriram Transport Finance of Rs. 2300 which has since been sold off and net cash realized. And therefore the net valuation of Stake held in Shriram Group is Rs. 3200 crores and not Rs. 5500 crores. And since in the end, to arrive at the valuation of lending business, we have taken the share market valuation as the parameter, therefore, you need to add this Rs. 2300 crores to the lending business valuation of Rs. 9500 crores taking the total valuation to Rs. 11800 crores which is a fair valuation of he lending business.

btw, just funnily enough, the rumour/grapevine going on in the market is that Ambani would not let his daughter cry with big tears and therefore, this Company is only facing some temporary valuation mismatch.

[…] What should I do with my holding in Piramal Enterprises – Link here […]

Stock is going down, old technique of dumping stock via posting irrelevant value in same

Regarding: Valuation of Healthcare business = Rs 700 Cr >>> This division was today sold for 950Million USD ( with stated equity gains of 2.3x investement. ). Where do you think was the gap in this analysis ?

Also Does the Pharma division evaluation need a relook ( considering the Valuation Piramal got for their previous pharma sale )

The premise of the entire article was to arrive at a bare minimum “sum of parts” valuation of Piramal Enterprises.

The DRG part was conservatively valued at a minimum of Rs 700 Cr.

The fact that it got sold for $950 Mn (not clear if this is equity value or enterprise value) is a good sign for Piramal Enterprises. They get more firepower to support the financial services business which is much more profitable and promising than the DRG business