IOL Chemicals has delivered some phenomenal performance over the last few years.

Profits of the company increased from Rs 5 Cr in 2017 to Rs 237 Cr in 2019.

Revenues increased from Rs 711 Cr in FY17 to Rs 1685 Cr in FY19.

Total debt has reduced from 447 Cr in Mar-19 to Rs 284 Cr in Mar-19.

On the back of such brilliant performance, the stock is trading at a PE ratio of 2.9. Compare this to the PE ratio of Dmart (113), Gillette (95), 3M India (75) the stock looks very cheap. The stock is screaming from rooftops – “BUY ME”.

Should we?

Let us investigate a little further.

What does IOL Chemicals do?

IOL is present in the Active Pharma Ingredients (API) and specialty chemicals space. It manufactures products like Ibuprofen which is used for producing pain killers and Metformin Hydrochloride which is used in anti-diabetic treatment. It also produces certain other chemicals like Ethyl Acetate, Acetyl Chloride, mono-chloro acetic acid.

The operating margins of IOL Chemical have dramatically increased from 9% to 31% in the last 3 years. Also, the company which was loss making in 2016 has managed to make profits of Rs 357 Cr in the trailing 12 months ended Sep-19.

Let us find out a little more from the credit rating report of IOL Chemicals dated 2nd Jul-19

http://www.careratings.com/upload/CompanyFiles/PR/IOL%20Chemicals%20and%20Pharmaceuticals%20Limited-07-02-2019.pdf

90% of the revenue of IOL Chemicals comes from just 2 products – Ibuprofen and Ethyl Acetate.

So, what has been the trend of the selling price of these two chemicals

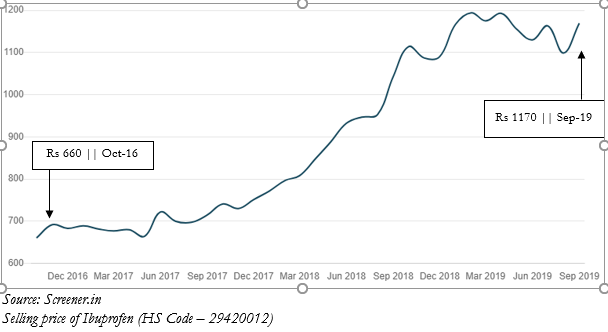

The selling price of Ibuprofen has increased from Rs 660 in Oct-16 to Rs 1170 in Sep-19 an increase of 77%.

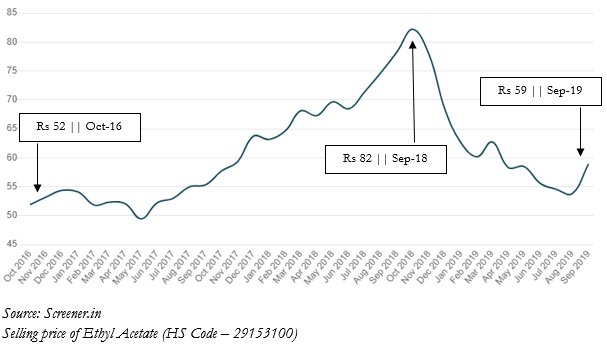

The selling price of Ethyl Acetate went up from Rs 52 per kg in Oct-16 to as high as Rs 82 per kg in Sep-18 and has now settled back to Rs 59 per kg in Sep-19

Clearly, the massive increase in the operating profit margins from 9% in 2016 to 31% in 2019 has been due to significant increase in the selling prices of its two main products – Ibuprofen and Ethyl Acetate which comprise (90%) of the revenues. We can also conclude that the prices of the raw materials used to produce these chemicals have not increased as much as Ibuprofen and Ethyl Acetate given the fact that operating margins have improved so much.

Now let us go back a little more in the past to dig out whether IOL Chemicals can sustain such high operating margins in the future as well.

We don’t have to go too far – Annual Report 2015

Revenue reduced by a whopping 32% in the year ended 2015

IOL Chemicals also suffered losses in the year 2015

IOL Chemicals incurred losses because of a mis-match in input and output prices.

What this really means is that IOL Chemicals was not able to pass on the reduction in end-product prices to the suppliers of its raw material. Clearly, IOL Chemicals does not enjoy “pricing power”. The company has to take whatever price the market is offering for its end-products and also pay whatever price is demanded by its raw material suppliers.

The situation was so bad that IOL Chemicals could not repay its loans and had to enter Corporate Debt Restructuring.

More specifically, the debt restructuring had to be done due to the economics of the Ibuprofen market changing

Can this happen in the future as well?

If for some reason prices of Ibuprofen and/or Ethyl Acetate reduce substantially, will IOL Chemicals be able to control raw material prices and remain a profitable company? Chances are that a reduction in selling prices of Ibuprofen and Ethyl Acetate will be a big shock to IOL Chemicals and at the least its profits will drastically reduce.

To check out the trend in the selling price of Ibuprofen, let us check out what one of the producers & consumers of Ibuprofen has to say about the demand-supply scenario and the price trend of Ibuprofen. Granules India uses the Ibuprofen bulk drug to prepare other formulations.

From the price graph for Ibuprofen mentioned above, we observe that the prices of Ibuprofen started increasing rapidly since around Mar-18.

Let us look at what the management of Granules India said on the investor conference for Q1FY19 dated 24th Jul-18

http://www.granulesindia.com/investor.php

One of the largest manufacturers of Ibuprofen – BASF has shut down its plant which has created a world-wide shortage of Ibuprofen. This is the reason for the significant increase in the prices of Ibuprofen.

Let us look at what has happened in the last 15 months,

Granules India Ltd – Q2FY20 Conference Call Transcript dated 23rd Oct-19

Several questions were asked about the pricing of Ibuprofen

Multiple times during the conference call, the Chairman & Managing Director of Granules India mentions that he expects the prices of Ibuprofen to reduce over the next several quarters.

He also mentions that there has been doubling of Ibuprofen capacity in India and now we are in a situation of excess/surplus capacity.

So, what is the reason for the stock of IOL Chemicals trading at a PE ration of 2.9?

The market has recognized that the prices of Ibuprofen will come down in the near future and correspondingly the profits of the company will reduce.

After IOL Chemicals had to enter corporate debt restructuring in FY15, the management has done well to improve the business operations. Around 2017, the management realized that environmental norms in China were tightening for chemical industries and hence there are likely to be supply disruptions/shortages in Ibuprofen. The cost of environmental compliance would require the Chinese players to invest in improving effluent treatment thus increasing the cost of production.

IOL Chemicals converted its multi-purpose plant to one which is capable of making just Ibuprofen in FY2017

This resulted in an expansion of Ibuprofen capacity.

The company aggressively expanded Ibuprofen capacity over the next two year to reach 12,000 TPA which is doubling production capacity in just 2 years.

Thus, the rapid rise in revenues of the company can be explained by 2 factors – doubling of production capacity for Ibuprofen and a 77% increase in the selling price of Ibuprofen.

With Ibuprofen prices expected to reduce due to excess production capacity in the industry, the profit margins of IOL Chemicals are sure to come down.

The general investor in this company without any specific knowledge of the chemical industry and the Ibuprofen supply chain in specific, can only take a wild guess as to how much the prices will reduce and where will the profit/loss margins settle at.

Investing in this company may turn out to be like driving in the night with the headlights switched off.

Disclaimer: Please do not consider this article as a stock recommendation. The article is an illustration of the kind of analysis that goes into fundamental research and equity investing. I do not hold the shares of IOL Chemicals.

Please consult your investment advisor before making any investment decisions.

The author (@amey153) is a SEBI registered Investment Advisor.

If you seek investment advice click here and someone from my team will get in touch with you within 48 hours

16 Responses

While I agree that IOL is greatly handicapped due to restrictive product ltd to two main product.The company is acutely aware of it and thus trying to diversify,Reason of 3 PE is well understoog else it should also demanding the PE similar to industry like Vinati Org, but comments like driving wothout headlights on, is extremely uncharitable and far from reality.As regards supply and demand BSAF production is slated for 2022 onward, it is well known fact. IOL is fully aware of it thus divesification, debt reduction, payment well before due dates and few other measures.at current price it is a loot.

Mr Dube,

The problem in the PE ratio is not the price, it is the earnings.

How sustainable are the earnings given the industry dynamics and the past performance of the company over multiple business cycles?

What will happen if for some reason on the future, the company repeats its 2015/2016 performance?

Why has Granules India exited the Ibuprofen manufacturing business even though Ibuprofen is a key raw material for Granules? Have they exited the Ibuprofen business at its peak?

These are some important questions we need to think about.

You are the best

When it will be in uptrend

When it will be in uptrend

Nice article. I think IOL management is fully aware of the situation. On positive side, they are actively pursuing debt reduction and diversifying their product portfolio. If they are debt free by the time ibuprofen prices drop, they would be able to weather the storm.

I liked your write up. Very detailed research done. With very good facts.

I would just like to point some things, which seems to be missed out.

1. One of the biggest issue I have seen in last 6 months was “VivaChem”. See the notes in previous quarterly results. Related party transactions.

It’s used for backward integration of Raw Material.

2. Well you have focused on Ibuprofen prices, BASF, Margins, Etc. When Ibuprofen prices were in uptrend, Company has built enough cash, assets and almost became debt free company. Don’t miss to give valuation to those cash generated and to assets built up.

1. Agreed – I have not done justice to the coverage of related party transactions in this article

2. What part of the cash reserves and other liquid assets will flow to the minority share holders?

Especially in light of the fact that there are significant related party transactions which may be detrimental to the minority shareholder?

What we have observed recently is that company has diversified it’s product portfolio in last 2 years. Which are again having very good margins.

So what I believe is that company has sucked all the honey and utilised it good way.

My only issue is Viva Chem

Mr Nagda

I think this is a key data point in the entire investment thesis.

Do you want to partner with a management with a “sense of stewardship” or are you ok with suspect related party transactions?

As a minority shareholder, will we ever know whether the large related party transactions are detrimental to the minority shareholders?

Why can’t IOL do the same work that Vivachem is doing?

What special expertise/technical know-how Vivachem has that IOL does not?

Good information..

I appreciate the analysis method advocated in analyzing with parameters like past,present and the future.Really wonderful work done by the group.Keep it up.My compliments with thanks to the entire team.

Same article written by Amey has been published in moneylifeI have gone through the article and after doing some independent research I have found some positive issues in relation to the company are missing which according to me are

1. It’s a debt free company that has a 35% worldwide market share in its flagship product exports of which generates tax free income and brings in ₹700 crore foreign exchange.

2. The report heavily relies on the opinion of the MD of Granules India Ltd which is a consumer of Ibuprofen (IOLCP’s flagship product). saying that the price of Ibuprofen has started falling but the report on the specialty chemicals sector by Emkay Global has states that the prices of Ibuprofen have risen during the past year, same view is endorsed by ICICI securities Moreover One of the largest manufacturers of Ibuprofen – BASF has shut down its plant which has created a world-wide shortage of Ibuprofen, the demand of the product is rising for which an additional supply of 1500-2000 MT would be required every year.

3. Why any company in the world would ever want to expand its commodity manufacturing capacity if the price of its product are falling.

4. The not dependent on two of its products but launching new products like metformin hydrochloride, lamotrigine, fenofibrate, clopidogrel Bi sulphate which are also high margin revenue.

5. There are several companies in the same vertical that are dependent on one or two products and have a PE of more than 20.

6. The article herein gives diametrically opposing view than that was published by Money life digital team on 19 Sept,2019.

Hi Mr Savla

1. Investment analysis is an opinion. What I have written above is my analysis about the company.

2. I have mentioned the good things about the company in the article, but I do focus on uncovering what is not very apparent

3. Moneylife is kind enough and mature enough to publish a counter-view (my article) in their magazine

4. Many times, the market is wrong in mis-pricing a stock, but on several other occasions the market is right and it is trying to tell us something. When other companies are trading at a PE ratio of 20, this company is trading at a PE ration of 3. The market does not believe the earnings to be sustainable. This is exactly what my finding is from multiple other source

Do make an informed choice and above all, the stock is not going to move up/down because I or someone else writes an article.

Very detailed analysis

Well Said IOLCP Profitability is linked to IBP Prices but Management has taken action like repayment of Debts by Mar 2020 Diversfication and a Fixed Deposit of Rs100 Cr as per Latest Q4 20 Results I agree with You One Should not Invest without Knowing Fact Same Happened with HEG and Graphite in 2017-2019 Now they are making Losses So Wise Investor Should take Limited Exposure