On 18th Jul-20, Central Electricity Regulatory Commission (CERC) came out with a draft regulation which suggested sweeping changes to the design of the power markets in India.

Draft Power Market Regulations (2020)

There is one very important proposal in this draft regulation that of “Market Coupling Authority”

Now, what is this “Market Coupling Authority” and what purpose does it serve?

An exchange serves the following two basic functions

- Order matching and price discovery

- Clearing and Settlement

The reason why IEX today is an impenetrable monopoly is because this “order matching” and “price discovery” happens at the exchange level. This means that both the buyer and the seller have to be on the same platform (either on IEX or PXIL) for their orders to be matched and get executed. Electricity buyers know that all the electricity sellers are on IEX and not on PXIL. Even if the buyers are willing to pay a very high price for electricity, they cannot buy it on PXIL because there are no sellers.

Same is the case for electricity sellers. The sellers know that all the buyers are trying to buy electricity on IEX. If the sellers want to sell on PXIL, they won’t be able to sell the full quantum even if they sell the electricity dirt cheap. It is a chicken and egg problem and IEX is a clear winner.

Now this function of “order matching” and “price discovery” will shift to the proposed “Market Coupling Authority”. This simply means that a buyer on PXIL will be able to buy electricity from a seller on IEX. He does not have to bother if there are sellers on PXIL or not. As long as he is willing to pay the price, he is assured of the transaction getting executed and his demand getting fulfilled.

In one stroke, the “competitive advantage” and the exact reason why IEX is a monopoly gets destroyed.Suddenly IEX is like Karna without his Kavach and Kundal – A formidable opponent but not an invincible one

At the price of Rs 181 on 29th Jul-20, IEX is trading at a PE ratio of 31.

A PE ratio of 31 does not seem to be expensive for a business which is an absolute monopoly with multiple triggers for revenue growth.

However, a PE ratio of 31 seems expensive for a business which is certain to lose its “monopoly” status sometime soon because of an impending regulatory change.

To understand the business better, do go through some of the other work I have published on IEX

- Article written by me on Moneylife Magazine on IEX India

- My presentation on IEX hosted on InvestingHub platform

If we want to invest in IEX, understanding “market coupling” is probably the most critical thing right now. It has far reaching implication on the business and its intrinsic value.

Now, let us try and understand why the regulator (CERC) wants to destroy the monopoly of IEX.

The Standing Committee on Energy evaluated the role, performance and functioning of the power exchanges and submitted its report to the Lok Sabha on 27th April 2016

Standing Committee report on functioning of Power Exchanges

The standing committee had this comment to make on the predominant market share of IEX

So clearly, the standing committee was not happy that one of the two power exchanges has complete market dominance. The reply provided by CERC was

Power Exchange was a very nascent concept in 2010. CERC did not want the fragmentation of volumes between several exchanges thus leading to an “inefficient” price discovery because of low volumes on either of the exchanges. CERC wanted only two exchanges to operate thus ensuring efficiency in “price discovery”.

CERC basically rejected the “observation” of the standing committee on energy that the rules and regulations favoured one exchange over the other. CERC in its response justified and reiterated the regulations that were in vogue.

In 2016, there was a petition filed by PXIL against the power system operator (POSOCO) because it wanted certain changes to be made in the methodology for allocation of transmission corridor between the two exchanges in case of “transmission congestion”

An expert group was constituted which gave its recommendations as under

The expert group unambiguously stated that “merging of bids” ie market coupling (what is proposed today in 2020) is THE solution to the problem of transmission corridor allocation between the two exchanges in case of congestion.

However, both the Power Exchanges opposed such a move

Even the Commission (CERC) was of the view that merging of bids leading the market coupling and common price discovery is not advisable at this stage of the market development

This means CERC again in 2016 dismissed the idea of “market coupling”.

We can conjecture that the reason CERC has been repeatedly rejecting the “market coupling” idea is because power exchanges are still a nascent concept in India.

Only 4% of the power traded in the country is traded on the power exchanges.

Most of the power bought and sold in India is using the rigid 25-year long term contracts. It doesn’t make much sense to introduce the concept of market coupling when only 4% of the power is traded on the exchanges.

So, what was considered “not needed” or even detrimental to the development of power markets in 2010, again in 2015-16 is suddenly now considered suitable and desirable in 2020. Why is that so?

Something must have drastically changed and that something is the proposal for market based economic dispatch (MBED). CERC put out a staff paper for discussion in 2018 on the topic of market based economic despatch (MBED).

The MBED (market based economic dispatch) proposes to shift the entire volume of the power sold in the country onto the exchange platform. Without going into the technical details of MBED, it suggests trading of 100% electricity (even that under long-term PPA) on the power exchanges. MBED will be a big step in development of power markets and has enormous benefits in terms of cost savings in power procurement because electricity will now be procured from the cheapest source at all times – something by design.

It was estimated in the staff paper that after implementation, MBED will result in saving of approx. 12% of electricity procurement cost (approx. Rs 62,400 Cr per year)

However, this proposal is extremely difficult to implement because it will require the amendment of all the existing 25-year PPAs (power purchase agreements). The players that need to agree to this proposal are all the state governments and all the existing generators that have a 25-year power purchase agreement (PPA).

When I first read this “staff paper” in 2018, I thought it is impossible to implement on the ground.

But, for a minute, let us forget the practicality of implementation and let us try and understand the depth of implications of the MBED proposal.

All the power buying/selling is expected to move to the power exchanges.

If we try and go into the background of the MBED, it will be a separate treatise in itself, but there are basically two reasons why such a radical proposal is being considered.

- Efficiency in power procurement and cost savings

- Solve the problem of transmission congestion and market splitting (during price discovery on power exchanges). Eg the cheapest power in India is available in Chhattisgar, Odisha and Jharkhand (large coal reserves). The far-away states like Maharashtra, Tamil Nadu, Punjab, Assam would like to buy all their power from these states and thus save huge costs. In such a scenario, the transmission corridor will prove inadequate and during the “price discovery” mechanism, different prices are discovered for different regions.

In this case, if multiple exchanges discover separate prices, it not only becomes chaotic, but a sub-optimal solution is reached.

In my opinion, this is the core problem that CERC wants to solve - Increasing share of renewable energy in the overall energy mix.

Especially the fact that since renewable energy is now cheaper than coal power, most of the capacity addition will happen through renewable energy. This necessitates a deeper and more liquid power market (all sorts of contracts day-ahead, real-time, capacity contracts, long-duration contracts etc)

The same paper also talks about the change in rules of operation for the power exchanges going forward.

Given the critical role that power exchanges will play after the MBED mechanism is implemented, it is but natural that the regulator would like to implement market coupling to remove the over-reliance for “order matching” and “price discovery” on only one of the exchanges.

Thus, we now start getting the reason behind why “market coupling” is thought about by CERC at this stage.

Given the enormous complexities, implementation of MBED will have to be phase-wise and probably voluntary for DISCOMs and existing PPA generators to start with.

However, within a time period of 2 years, the volumes traded on the power exchanges will increase by at least 5 to 10 times.

That brings us to what the Power Secretary – Sanjiv Sahai said in a webinar arranged by The Energy Resources Institute on 21st Jul-20. Watch the clip from 01:22:00 for 90 seconds

Sanjiv Sahai at the TERI organized webinar

To quote Mr Sahai – “Something is going to happen in the next 4 months, a big policy change, which will make the day-ahead and real-time markets far far more liquid”

My guess is that this “big policy change” that the Power Secretary referred to is MBED.

Market-based economic dispatch will be the biggest reform in the Indian Power Sector after the Electricity Act 2003. It is not only very difficult to get the political buy-in from all the stakeholders, but given the complexities and intricacies involved will also be a mammoth effort to get it implemented.

However, the present government has a history of getting changes implemented which were in discussion for decades – GST, Insolvency and Bankruptcy code, Coal Sector privatization, abolition of APMC act, National Education Policy, labour law rationalization (partial) and the list goes on. If it is deemed important and useful it seems that after 30 years (since 1991) only this government has the political capital and the political will to get complex and difficult reforms implemented.

To summarize,

- The concept of market coupling will basically destroy the “competitive advantage” and the very basis for IEX being a monopoly

- What is the motivation for CERC to come up with such a proposal?

CERC wants to implement MBED which will result in a massive increase in the volumes traded on the power exchanges

The 4% of market share of power exchanges may easily become 40% in a 2-3 year time frame

Why do I think that market coupling authority is one of the steps towards the implementation of market-based economic dispatch (MBED)?

It is about what Sherlock Holmes says – don’t just look at what the evidence is, also look at what evidence is missing.

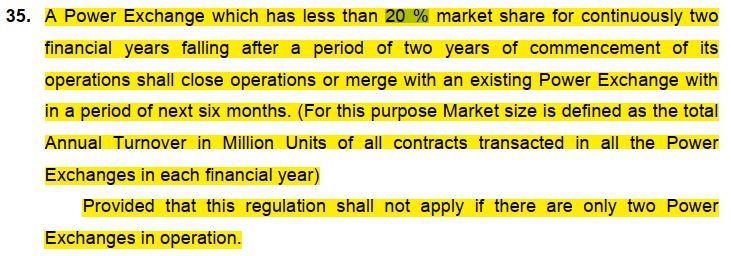

Power Market Regulations 2010

India went in for a privately-owned multiple exchanges model in 2010. Since the power sector was in a nascent stage of development, CERC did not want too much fragmentation in volumes traded on the exchanges. Hence the proposal to restrict the competition to just two power exchanges and the compulsory merger of the third exchange in case it has less than 20% of the volumes traded.

This provision is missing from the Draft Power Market Regulations 2020. Why?

I am guessing that there are two reasons

- With MBED the volumes traded on the power exchange would multiple by a HUGE factor. There might be scope for 3/4/5 power exchanges to operate.

- With “order matching” and “price discovery” happening at the level of the market coupling authority and not on the power exchange, the problem of non-uniform price discovery between the multiple exchanges goes away.

There is another provision which was missing in the 2010 version of the Power Market Regulations, but is present in the 2020 draft.

The Power Exchange will have to get the maximum transaction fee that it will charge approved by CERC. Crucially this provision was not mentioned in the 2010 regulations. Since very little power was traded on the Power Exchanges, there was no need to regulate/approve the transaction fees charges by the Power Exchanges then.

It seems that if a majority of the power is routed through the power exchanges by design, CERC now would want to have some sort of regulation on the prices being charges by Power Exchanges.

If we go back the 2018 staff paper on market based economic dispatch, the paper mentions this point as well.

We need to also appreciate that the Draft Power Market Regulations 2020 talk about market coupling only for day-ahead and real-time markets, not for the other types of contracts term-ahead, long-duration forward contracts or capacity contracts (which are currently only in the cradle with no liquidity and no precedence in India).

The dots seem to now connect.

Here is what I think of the entire episode

- With the implementation of the concept of “market coupling authority”, the impenetrable nature of the IEX monopoly will be destroyed.

- Will the power exchange market become like the stock broker market? With hundreds of players competing with each other and some of them even offering zero brokerage like Zerodha, Upstox etc.?

I think the power exchange market will become like the credit rating market. May be 3-6 players with IEX retaining the dominant position (like CRISIL) - If market coupling is introduced at all, it will be alongwith MBED which will also result in an exponential growth in volumes traded on the power exchanges.

- In my opinion, CERC does not want to “harm” the monopoly of IEX, but if MBED in introduced it will want to make sure that the “market-design” is proper and ensures “social welfare maximization”

- What about transaction fees? Will there be a downward pressure because of competition between power exchanges?

Let us think from the perspective of a buyer.

Power purchase cost ~ Rs 4.00

Transmission Cost (inter-state) ~ 50 paise

Transmission Losses ~5% which is 20 paise

Intra-state transmission charges ~ 50 paise

Intra-state transmission losses ~ 5% ie 20 paise

Total cost of power purchase = Rs 5.40

Fees paid to power exchange = Rs 0.04 = 0.75% I estimate (and I can be completely wrong about this) that the power exchanges will try and compete on customer services, relationship, ease of use etc. instead of trying to lower the transaction fee for the buyer/seller and lure them. The cost saving is just not that high. However, there are only 55+ distribution companies in India and it may not be very difficult with intense business development efforts to woo at least some volume away from IEX.

What will happen after market coupling and MBED is implemented?

There will be a sudden jump (500%/1000% in a short period of say 24 months). IEX revenues (assuming no reduction in transaction fees) will increase by a factor of 2 to 5 times.

However, IEX monopoly will be destroyed. Also, future growth after that will be muted because pan-India electricity demand increases by 4% to 5% per annum. When 50% of the total electricity is traded on the power exchanges and more players want to enter this business, the growth for IEX after that will be mediocre.

This means no one would want to pay a PE ratio of 30 for IEX and the PE ratio would probably drop to 15 – suggesting a steady state low growth stock.

What may happen is MBED and market coupling are not introduced because it is too complicated?

Recently, the ministry of power has approved the introduction of forward electricity contracts on the power exchanges.

This along-with other forward-looking reforms and the fact that renewable energy is becoming a big part of the energy basket which necessitates a lot of changes in the way power is procured (beneficial for power exchanges) will result in a handsome growth in revenue/growth for IEX. Already, real-time market seems to have boosted volumes (and revenue) by 20% for IEX.

What will be a negative trigger?

Introduction of market coupling without a clear and aggressive implementation schedule for market based economic dispatch (MBED). This will be detrimental and the stock may fall by 30% to 50%.

Depending on the exact proposal, this could either be a signal to exit the stock or an opportunity to buy more. We will keep a close watch.

IF YOU WANT TO SEEK INVESTMENT ADVICE CLICK HERE AND SOMEONE FROM MY TEAM WILL GET IN TOUCH WITH YOU WITHIN 48 HOURS.

10 Responses

Awesome write up Sir !!!

Very well thought out and articulated piece. I had a few questions though:

1) Seems to me that MBED obviates the requirement for signing a long term PPA if prices are going to be determined daily on an exchange. Gencos look for price security before investing significant capital in setting up capacity. If they dont have price security through a PPA, would they set up new capacity and will banks lend them money? Given 175 GW of new renewable capacity has to be set up over the next few years, isnt this a serious disincentive?

2) Why does MBED even need to be implemented? Given increasing share of renewable generation and the associated intermittency in supply, isnt power demand inevitably going to shift to exchange? We have seen this in Europe where regions with higher renewable capacity have higher exchange traded demand. For example, Nordpool has 90% of demand traded on exchange beacuse 60% of generation is through renewables. Seems to me that this regulation is unnecessarily intervening in the natural order of things. Europe does not have MBED yet has high exchange traded volumes.

3) It seems that the market coupling authority (MCA) is going to be state owned given the need for an independent platform . We have all seen the track record of state owned entities in numerous other sectors. Given that exchange traded market is just 4%-5% of overall demand, there is a clear need for an efficient exchange which can ensure security,quality service and product innovation, in order to aid market growth. Given IEX’s track record across all these fronts and the lack of ability of a state owned entity to do so, is there a need to set up a separate MCA to cater to domestic demand?

4) I think Europe is a great example to look at, given its the most developed exchange market in the world. All the regional markets have separate exchanges which cater to domestic demand. Each exchange is the monopoly in its domestic market given that greater liquidity leads to lower costs. However, for cross border trading, in order to aggregate separate demand supply curves received from various exchanges, an independent MCA has been set up. There is no market coupling for domestic markets. Isnt this the example which India should also follow, given the obvious success which Europe has enjoyed?

Would appreciate your thoughts on this. Thanks.

Thank you for this excellent Amey Kulkarni and for linking the dots.. Highly appreciated sir

Great article! You explained everything very clearly.

Well sir, Lets see even if the MBED is implemented we can expect the market share of IEX to be atleast 50% on the other side the transactions are expected to atleast double.

This is a business of operating leverage and the jump of transactions by a factor of 2 will increase PAT by more than 100%.

Effectively the PE of 30 now will become 15 on the back of earnings growth and further valuations will depend on how the Industry evolve

Hi Amey, in the blog you mentioned “let us keep the practicality of implementing this MBED aside” – isn’t that the main bottleneck? The implementation of it. Would this not be renegotiation/cancellation of LT PPA contracts, which the SC did not allow for AP govt. recenty. Many thanks.

Hi Pratik

The point I wanted to highlight was that market coupling does not make sense without MBED (market-based economic despatch) and it may not be introduced unless MBED is also implemented simultaneously.

Yes, there are huge contractual/legal/co-ordination issues with implementation of MBED.

The government will make enabling legal and regulatory provisions so that it stands in court.

Essentially none of the contracts will be reneged. The DISCOMs will continue to pay the capacity charges. Its only the way in which power is scheduled for despatch will be changed.

Also, payment will continue as before (some adjustments in the mechanism not amounts will have to be made)

the beauty of the MBED is that the existing contracts will be honoured. If the Discom gets a lower price based on marginal cost than his PPA price, the generator won’t be scheduled and the generator only gets the capacity charge. But if the price discovered by the Market is higher than the PPA price, then the genco refunds the excess. So, the Discom is sufficiently protected. This improves the overall cost efficiency of the entire power sector without compromising the grid safety. Most important think to watch out is that the Exchange can become a trader if the market coupling operator concept is introduced. For instance, PJM, NyISO are all not for profit. So, the volumes can be there but the pricing might be significantly lower. Net net very high uncertainty.

Hi Amey,

Thank you for this detailed article to help clearly articulate and explain investment rationale on IEX, with unbiased views.

I have gone through your webinar / video on IEX investment thesis in investinghub and it has been an amazing content to learn and decide on IEX investment.

I have learnt that CERC will be implementing MBED effective 1st April 2022.

https://economictimes.indiatimes.com/industry/energy/power/market-based-economic-despatch-phase-i-to-begin-from-april-1-2022/articleshow/86865106.cms

I have also gone through the latest IEX investor call transcript, where there have been discussion about how MBED may impact IEX business.

With my limited understanding, MBED is being implemented from 1st April 2022, mandating inter-state generating stations, to start with, to mandatorily sell power on Power Exchanges – WITHOUT MARKET COUPLING.

Few questions, if you could help us in understanding, please (Assuming mock drills go well and MBED will indeed be implemented from 1st April 2022):

1) What volume increase do you foresee, if all inter-state generating companies come on to power exchanges for selling?

2) Is it correct that the MBED is being implemented without “Market Coupling” being implemented?

3) What are you other critical thoughts about MBED getting implemented from 1st April 2022?

It has been an amazing learning from you on IEX, in particular, and Power Sector, in general.

Thank you.

Based on recent announcement by power ministry, they want to implement power coupling mechanism, what is your take on that news considering iex price already fall by22%