Medi Assist Healthcare Services Limited, is a holding company with a rich history dating back to 2000, which provides third party administration services to insurance companies through wholly owned Subsidiaries, Medi Assist TPA, Medvantage TPA (from February 13, 2023) and Raksha TPA (from August 25, 2023).

A third-party administrator is an organization that processes health insurance claims for insurance companies and provides services such as policy administration, customer service and network management.

Some Benefits of leveraging TPA functionalities

For Insurers

- Operational Efficiency & Cost Saving: By outsourcing claims processing and administrative tasks to Third-Party Administrators (TPAs), insurers can focus on core activities & hence can achieve significant cost reduction.

- Fraud Prevention & Real Time Analytics Dashboards: Enable TPAs to monitor patterns and anomalies in claims data, ensuring that only legitimate claims are processed.

For Healthcare Providers

- Streamlined Billing: TPAs simplify the billing process for healthcare providers by handling claims submissions and payments, reducing administrative burdens and ensuring accuracy.

- Increased Patient Volume: Direct policyholders to network providers, which increases patient volume and revenue for healthcare facilities.

- Handling Complexity: As insurance companies introduce new and innovative policies to differentiate themselves, the complexity of managing these policies increases. Rather than Hospitals managing these complexities TPAs can take care of these overhead.

For Policy Holders

- Improved Customer Experience & Transparency: TPAs offer transparent claims processing, providing policyholders with real-time updates on their claim’s status.

How TPAs make money??

- Contrary to common belief that TPAs only charge during claim reimbursement or processing, in reality TPAs charge a flat % charge to Insurers on the premium managed or say PUM (Premium Under Management). PUM (Premium Under Management) are charged/collected by Insurers who are clients of TPAs like Medi Assist.

- In Medi’s case, it charges ~2 – 5.5% flat commission fees depending upon the product type it is supporting. For FY24, PUM for Medi Assist was 19050 CRs and the revenue for the corresponding year was ~640 Rs, so if we oversimply, the yield for Medi Assist was ~ 3.3% (640/19050).

- So, as the medical inflation keeps on increasing, Premiums collected by Insurers are bound to increase year on year and hence will be resulting in increase of TPAs revenue.

Prospects of HealthCare & TPA Industry

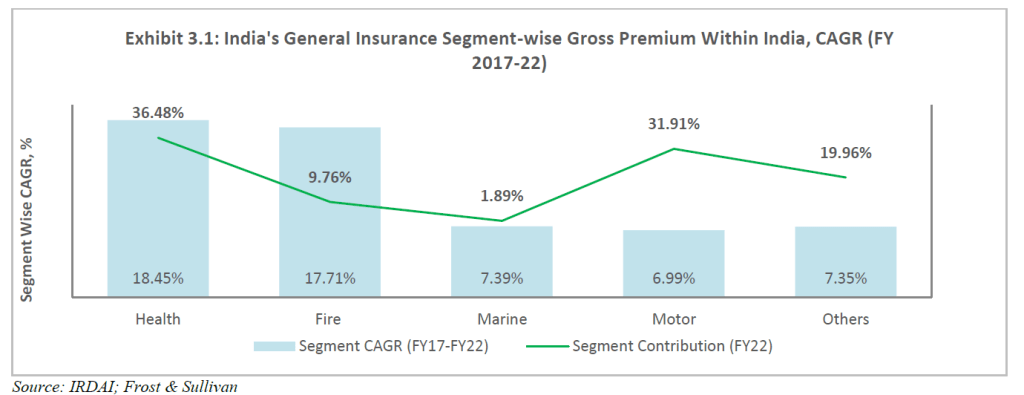

- Health Insurance was the largest and the fastest growing insurance segment in the general/ non-life category between 2017-2022 period. Seems will be the case for upcoming few years as well as the medical inflation is almost > ~10% range (double of general inflation rate (CPI).

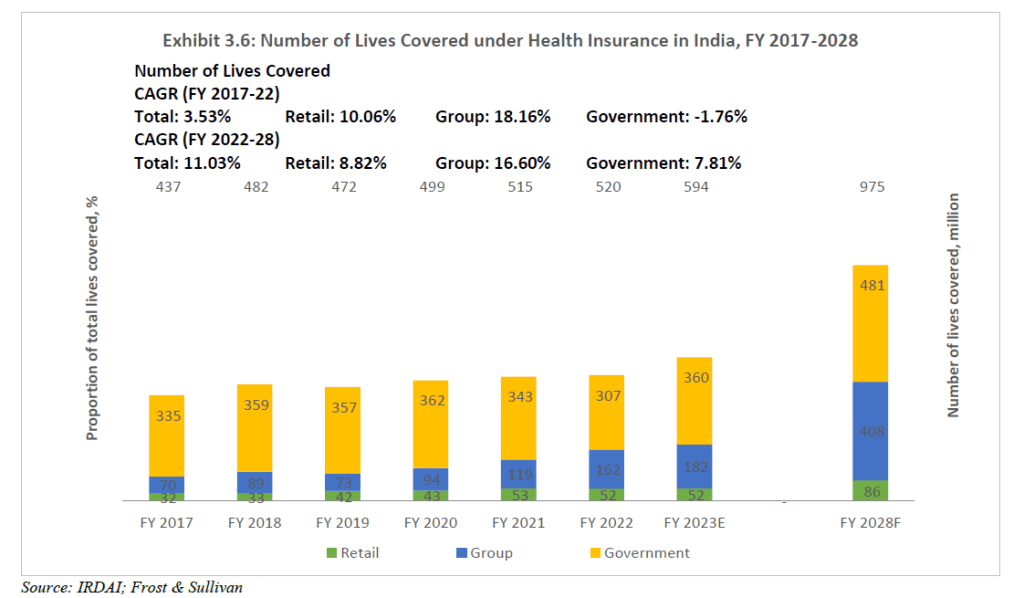

- Proportion of Lives covered under Health Insurance in India is still < 25% excluding Govt Schemes which leaves a long runway for growth (as forecasted), as people simply will not be able to bear expensive medical expenses out of their Pocket (OOP) for a longer time.

Long runway for Retail and Group segments Health insurance penetration.

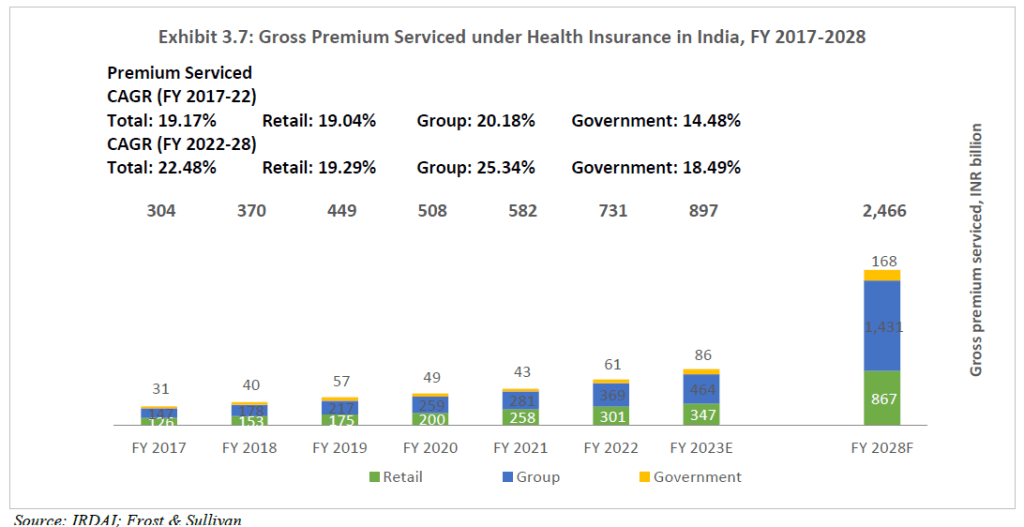

- Gross Health Premium Serviced increased ~19% year-on-year across Retail, Group, and Government segments. And forecasted to grow at faster pace for Group Segment followed with Retail Segment. This is an excellent news for TPAs which dominate this space especially Group segment.

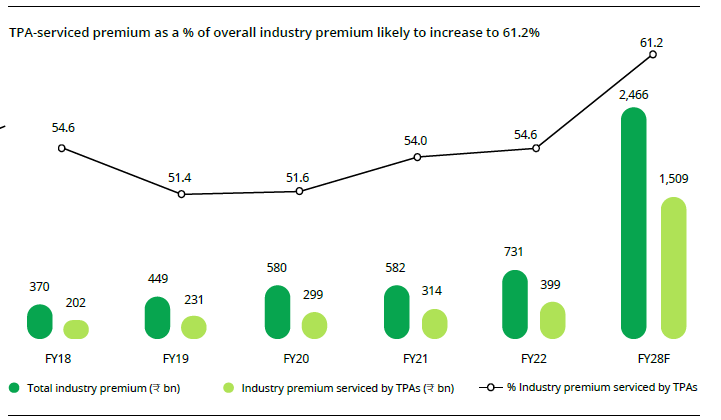

- TPA-serviced premium as a % of Total premium forecasted to increase from current ~53% to 61% by FY28 because of increase in the volume of claims and the complexity of products.

Again % increase for Group expected to be much higher than overall industry, big benefit for TPA industry growth.

So, from Industry Growth perspective, considering the current low penetration of people covered under health Insurance, Health Insurance industry has long tailwinds which is forecasted to grow at ~20% CAGR for next couple of years & hence for TPA industry.

Additionally, Group (~29%) and Retail (~20%) Insurance segments are set for faster growth rates among the sectors which are the preferred play areas for TPA players.

So, Industry prospects look reasonably bright..

But what about Medi Assist’s capability & Prospects, let’s try to address those?

Let’s see how Medi Assist Healthcare Services has been performing on our various parameters.

1. How has been the Business Growth & Profitability?

By leveraging synergic acquisitions from time to time, company has grown its revenue at ~18% for last 5 years by maintaining margins of >22%. Profit Margins at around 10-12% and Profits have grown at ~20% during same period.

Company has mentioned time to time that ~22-24% margins are sustainable on long term basis and might fluctuate a bit for some quarters during acquisition migration period.

As Medi Assist major revenues are take rates/yields (normally ~2%-5.5%) from Premium Under Management (PUM), PUM has grown at ~30% CAGR in last 3 years which is one of the critical growth parameters for growth. Yields are normally on ~3.3%.

Works on NEGATIVE working capital days as collects fees upfront from Insurers for the Premiums under management in the start of the tenure itself.

2. Does Medi has Leadership Position? What about its margins, Client Retention rates etc?

- 19.6% Leadership Position in Health Insurance (Group + Retail) Premium managed. Post Paramount acquisition completion (currently waiting for IRDAI clearance), this is scheduled to increase to ~23.6%.

Within TPA Service Revenue, it’s leading current market share with ~30% will further expand to ~36% post Paramount acquisition.

2nd position TPA (Vidal ~13% market share within TPA service) doesn’t have even half the market share of what Medi Assist has.

- Margins & other financial parameters of Medi Assist are way higher than their current competitors. As per management, whole credit for this goes to their Tech estate/Platform which is scalable and can be seamlessly integrated post acquisitions. As a result of this, post 3-4 quarters of acquisitions, their new acquisitions start operating with margins ~21-24% which is best in the industry.

- 95% Client Retention rates within group segment and majority of the Group clients are with Medi Assist for more than a decade, so its highly likely the same to continue.

- Cost Leadership, between FY21 and FY24, the total number of claims intimated to Medi Assist grew from 3.1 million to 7.63 million, all this was supported w/o corresponding increase in employee strength. Though as company mentions, they will stick to 40% Employee Expense rate of Total Revenue.

- Tech Focus offering to strengthen the reliability and integrity of claims processing by augmenting inhouse fraud detection capability and associated savings.

- In house Raksha Prime product enabled Patients (~65000 till now) to walk out of the hospitals immediately after doctor’s discharge, without waiting for discharge formalities, powered by proprietary AI technology for accurately predicting claim approval amounts. Results in saving of up to 6-7 hours. Can be a game changer for hospitals and patients if able to scale successfully.

3. What about the Management? Are they competent and have execution history?

- Capable Management, Chairman Dr Vikram Chhatwal initial promoter has been with company since early days of operations. And current CEO, Satish Gidugu has been with company since 2013 first as in CTO then as CEO lately. Prior to that he has been with RedBus for ~3 years as CTO to ensure high availability/reliability on cloud infra which explains his inclination towards Tech enablement.

- MediAssist is more a Tech company rather than a simple vanilla TPA, and all the credit for 20%+ sustainable margins goes to their Tech Estate and hence if a CTO from engineering background is becoming a CEO, this speaks a lot about the Tech/Engineering Culture on which Medi thrives. It is also evident from the way CEO responds in all the quarterly concalls.

4. Has this TPA industry played out somewhere else on this planet earth?

- In US, Total Direct Health Insurance Premium written in 2023 was ~1.4 trillion USD and corresponding TPA market size/revenue was valued at ~158 billion USD. So, TPA market size in US is ~11% of total Direct Premium (158/1400).

- On similar note if we compare for Indian markets, as per IRDAI, total Health Insurance written for year 2023 was ~97880 CRs. Out of this, TPA market revenue was ~2000 CRs. Likewise, the TPA Market size in India is ~2% (2000/97880).

- So, in future, can Indian TPA market revenue increase from current ~2% to ~5% of Total Insurance Premium which is currently 11% in US?

5. And Not So Good Answers – Key Risks / Weaknesses

- More Insurers opting for Inhouse TPAs rather than outsourcing to save the ~3-5 % cost. Though company management is confident about, this will not be as such threat for Medi Assist. As this threat has always been existed and seems because of their offerings of the technology, the access, the cashless facility & predictably management, they have been with almost all 27 Insurers in Group Segment with ~95% retention rates. Not only that, they were able to increase market share as well.

- Top 5 Client revenue concentration risk as revenues more than 75% for top 5 clients.

- Dependency on acquisitions to increase Market share which always exposes to various other acquisitions associated risks like margin contraction or say Employee expense increasing etc. Till now acquisitions have been done in ~2 times of the sales whether for 120 CRs for Raksha or similarly planned for ~300 CRs for Paramount. On a similar note, Bajaj Finserv’s acquisition of Vidal with ~200 CRs revenue for 325 CRs looks to be on lower range.

- Yield reduction on PUM serviced (from current ~ overall 3.3 %) because of Industry consolidation or intense competition from big corporate house like Bajaj Finserv acquiring 3rd largest TPA by Market share, Vidal.

- Simply put it’s not always necessary that every decent business must be a decent investment. This is one of its first kind listed in Indian Markets and TPA industry can still be considered at its very nascent stage. So, need to see if the Mgmt walks the talk of their aspirations like PUM expansion, Sustainable Margins of ~22-25% along with extending their leadership position.

6. What about Stock Price? Expensive, Cheap or Fair ? Valuation

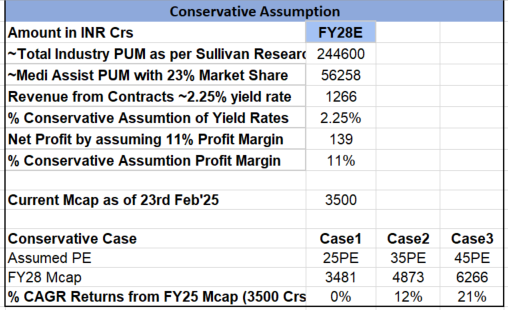

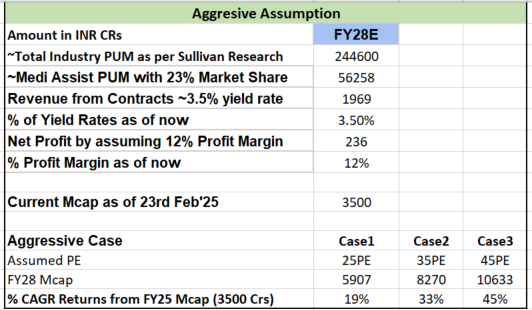

- As of 23rd Feb’25 , with MCap of ~3500 CRs and Net Profit of ~83 CRs (with 24% Tax Rate) , its trading at ~43 PE multiples. As we don’t have any other TPA listed in our markets we won’t be having as such benchmark to compare.

- By keeping things very simple, post Paramount acquisition, total market share will be ~23 %. Let’s try to extrapolate the revenue/Net Profit for year FY28 as we have possible rough estimate of PUM for FY28 from Frost and Sullivan Research report.

- Conservative Case by assuming the same Market Share as of today post Paramount acquisition which is ~23%, yield rate of 2.25% lower than usual 3.5% & with NPM as 11% against 12%.

- Aggressive Case by assuming current Market share ~23%, yield as 3.5% and NPM as 12%.

Conclusion

So, to conclude, considering the company’s current market leadership, competitive tech offering, sustainable margins, capable management along with long persistent industry tailwinds in Healthcare/TPA sector. It seems :-

- Probability of Occurrence of 15% CAGR returns in next 3 years looks VERY HIGH.

- Probability of Occurrence of ~20-25% CAGR returns in next 3 years (~stock price to double) looks moderately HIGH.

Having said that, in investing anything which can go wrong sometimes indeed go wrong 😊.

Analyst @ CandorInvesting

Disclaimer:

Registration granted by SEBI, membership of BASL and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. Investment in the securities market is subject to market risks. Read all the related documents carefully before investing.

This blog post is just for educational purposes and not a stock recommendation.

SEBI Registration Details – https://candorinvesting.com/sebi-registration-information/

Disclaimer – https://candorinvesting.com/disclaimer/