This article was originally published in the Moneylife Magazine in November – 2019.

https://www.moneylife.in/article/could-investors-have-sidestepped-the-75-percentage-crash-in-va-tech-wabag-stock/58642.html

VA Tech Wabag is a very reputed name in the water treatment, sewage treatment, sea water desalination fields. The company operates in 20+ countries. It has completed more than 6000 projects so far, has 3 R&D centres across the globe and has more than 100 patents to its name.

But, why has the stock crashed by 75%+ in the last 5 years?

The VA Tech Wabag stock was trading at a price of Rs 827 in Nov-14. On 8th Nov-19, it closed at a price of Rs 177.

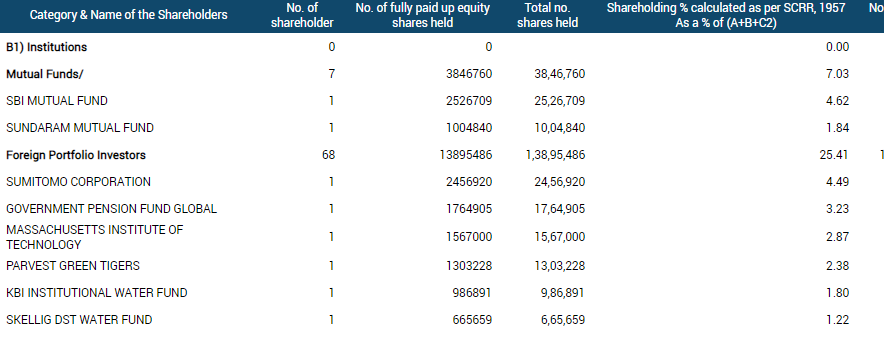

VA Tech Wabag not only enjoys a pre-eminent position in the water treatment industry, it also has some large institutional holding.

Mutual Funds like SBI, Sundaram hold shares in the company. Large institutional investors like Sumitomo Corporation, MIT college endowment fund, Vantage Equity Fund hold a significant position in the company.

The management of VA Tech Wabag has a good reputation.

It is well poised to take advantage of the Namami Gange (Clean Ganga) mission and the overall push towards river revival, sewage treatment and clean drinking water on a pan-India basis.

More than 60% of the revenues of the company come from projects executed outside India and the company’s order book has been steadily increasing.

The order book stands at more than 3 times annual revenues.

However, after falling from Rs 827 in Nov-14 to Rs 303 in Sep-19, the stock has fallen by another 40% just in the last 2 months.

What went wrong?

Could the investor have predicted the decline in the stock price of VA Tech Wabag and got out of the stock in time?

Let us investigate further.

The first thing to check if everything is ok with the company is to check the operating cash flow

- VA Tech Wabag has reported a negative operating cashflow in 4 out of the last 8 years.

- The company has reported a cumulative PAT of Rs 815 Cr in the last 8 years.

- However, the cumulative operating cashflow is a negative (-382) Cr in the last 8 years.

- The company is not able to convert reported profits into cash.

What is the cause of the poor operating cashflow?

For an EPC (engineering procurement & construction) company it is usually the receivables

* Due to change in Accounting Standard 115, certain receivables have been reclassified as “Dues from customers for construction contracts” by the company. For our analysis purpose, we will treat them as receivables since this money has not been received yet by the company.

Receivable days has been very high for the last 8 years. VA Tech Wabag takes 300+ days (10 months) to collect money from its customers after the bill for the completed works is presented.

Consequently, the borrowings have also increased over the years.

Debt to Equity ratio has deteriorated from 0.2 in 2012 to 0.6 in 2019 – though it seems to have not reached an alarming level yet.

Total Debt (Rs 613 Cr) is much lower than the receivables (Rs 2542 Cr).

How is the company funding its working capital requirements (receivables) if not by borrowings?

It is evident that VA Tech Wabag is funding its long receivables cycle by delaying payment to its own vendors. A vendor (sub-contractor) looking to take up a new job with VA Tech Wabag in 2019, can expect to receive his payments with a delay of 7 months (221 days) after he has completed his job and raised the bill. A vendor/sub-contractor who does decide to take up the job will be either desperate for business or will do so at a much higher cost after accounting for the financial costs of the delayed payment.

Let us try and probe a little more about the trade receivables.

From note 7 to the consolidated financial statement, we observe that

Typically trade receivables are due within 30/60/90 days of presenting the customer with the bill. However, a significant amount of Rs 127 Cr is mentioned under the head non-current receivables. To begin with, the company expects this money to be realized after 12 months.

Let me also draw your attention to note 12 of the consolidated financial statements

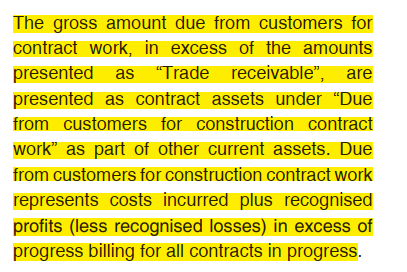

A massive amount of Rs 1192 Cr is “Due from Customers” as of Mar-2019.

What is this “Dues from Customers”?

“Dues from customers” is unbilled revenue – the company has completed the work, but has not yet presented the bill to the customer. This looks preposterous.

In fact, the “Dues from customer” asset also includes the revenues and profits that have already been recognized in the P&L statement even before the bill has been presented to the customer.

Extract from note 3.4 to the consolidated financial statements

“Unbilled Revenue” is not a very uncommon thing for EPC companies, however such high levels of both trade receivables and unbilled receivables looks a little problematic.

Let us turn our attention to customer retention money. Usually in an EPC contract, the customer retains a certain percentage of the contracted amount – usually 10% for a period of time – to cover for the defect liability period. This is usually done so that the contractor (VA Tech Wabag) will rectify any defects that arise within a reasonable time period after commissioning of the project. The defect liability period varies depending on the type of project, but we may estimate it to be say about a year. The project then enters a phase of operation & maintenance.

However, for VA Tech Wabag, the money that customers have retained with themselves has significantly increased in the last 7 years

Customer retention money has increased by 4 times from Rs 125 Cr to Rs 553 Cr o 2019, whereas sales (projects executed) have hardly doubled in the last 8 years.

Let us turn our attention back to note 12 to the consolidated financial statements

Direct Adjustment with retained earnings

Extract from the note 34 of the consolidated financial statements.

The contract balances stand at Rs 1192 Cr as on 31st Mar-19. This is the “Dues from customers” we saw above in note 12 to the consolidated financial statements. During the year FY19, Rs 369 Cr of the Contract Balances were billed and moved to “Trade Receivables”. However, Rs 163 Cr were written off as allowance for expected credit losses. This was even before any bill was raised to the customer. Also, let us check what were the bad debts written-off in the profit and loss statement.

Extract from note 31 to the consolidated financial statements.

We observe that the bad debts written-off in the profit and loss statement in the entire year were only Rs 92.5 Cr. Thus, the expected credit losses under “Dues from customers” which were Rs 161 Cr have not passed through the P&L statement.

Profit before Tax in FY19 was Rs 110 Cr. If this Rs 161 Cr was charged to the P&L statement, the company would have had to report losses.

Apparently, this direct adjustment to retained earnings without mentioning this write-off in the P&L statement has been going on for some time now. VA Tech Wabag wrote-off Rs 172 Cr, Rs 121 Cr, Rs 138 Cr, Rs 131 Cr in the year 2018, 2017, 2016, 2015

Let us come to the last piece.

Let us look at note 46 to the standalone financial statements

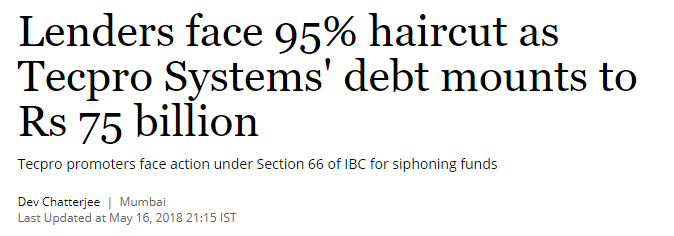

Dues from a project in consortium with a bankrupt company – Tecpro Systems

This is a well-known issue by the investors of VA Tech Wabag as the origin of this matter dates back to 2010. However, one needs to put this piece of information in perspective when analyzing the company. Rs 416 Cr is yet to be received for a government contract executed long back. What is more, Rs 69.5 Cr needs to be recovered from Tec Pro Systems – a company which has gone bankrupt.

Tecpro systems has not only gone bankrupt, it is also alleged that the promoters have defrauded and tried to siphon off money.

Final resolution of Tecpro Systems came on 15th May-19

http://www.tecprosystems.com/forms/Final_order_of_NCLT_dated_15.05.19.pdf

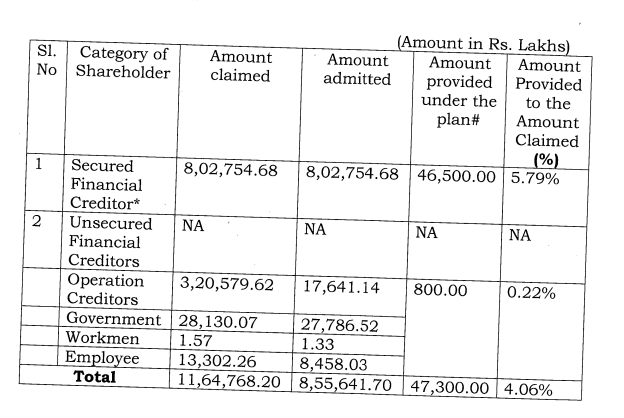

The secured creditors of Tec Pro systems will receive only 5.8% of their original (equivalent to interest earned in 6 months). The operational creditors (VA Tech Wabag is one of them) will receive only 0.22% of the original amount.

Actually, as per the corporate resolution of Tecpro Systems, the operational creditor claim of VA Tech Wabag has already been rejected by the insolvency and resolution professional.

http://www.tecprosystems.com/forms/Opertational_Creditors_of_Tecpro_Systems_Limited_2nd_May_2018.pdf

The claim of Rs 588 Cr of VA Tech Wabag has been rejected by the resolution professional. The company will probably get directly paid Rs 416 Cr directly the government agency (APGENCO). However, at least the Rs 42 Cr being recovered from Tech pro systems will have to be written off.

Its amazing how much information one can get by a simple reading of the annual report of a company and a little bit of google search.

Like human beings, businesses have their own good times and bad times. Sometimes, the economy, competition, interest rates, GDP growth etc. will be favourable and sometimes not. However, companies that hide the reality from the investors through accounting “adjustments” are hiding the truth from themselves.

Buy and hold fundamental investors typically have an optimism bias. They believe that if a stock they hold is down, it is only a temporary phenomenon. With time, when the economy recovers, stock markets recover, their stock will also eventually go up.

However, buy and hold does not work, investors need to adopt the buy-check-hold strategy.

If you want to learn some forensic accounting yourself, check out my workshop on “Forensic Accounting for Investors”

Please do not consider this article as a stock recommendation. The article is an illustration of the kind of analysis that goes into fundamental research and equity investing. I do not hold the shares of VA Tech Wabag.

Please consult your investment advisor before making any investment decisions. The author (@amey_candor) is a SEBI registered Investment Advisor.

8 Responses

Thanks for the post. Really very useful..!!

We are the leading Watre Treatment Plant Manufacturers in Chennai, Visit our website

Manual Multiport Valve Manufacturers in Chennai

Dosing Pump Manufacturers in Chennai

Cartridge Filter Housing Manufacturers in Chennai

Reverse Osmosis Manufacturers in Chennai

Water Softening Plant Manufacturers in Chennai

Iron Removal Plant Manufacturers in Chennai

Hi Amey, thank you for your cast studies, it provides a good ground of frameworks to look at things.

Regarding ‘adjustments via retained earnings’ – how is this captured in the Annual Report? Do you infer it just be seeing the difference between ‘provisions created in BS’ vs ‘provided for in P&L’?

Many Thanks,

Pratik

Pratik

This will usually be covered under a separate notes to accounts.

Usually check the note “Share Capital”, additions/adjustments to reserves and surplus.

Hi, so in FY19 annual report under ‘share capital’, there is one 180 crore adjustment due to Ind AS adoption. Do not see any such adjustments in FY18 or FY17 Annual Report. If you can help me with the same. Many thanks in advance.

Regards,

Pratik

Good analysis. So PAT of this co. Is misleading. But i am interested to redraw P&L to know if business is profitable at all.. any pointetscwill be very helpful..

Look at all the adjustments they have made to the (trade receivables + customer advances) over the last 10 years.

Deduct it from the PBT and you get the re-drawn P&L statement

Hindustan Unilever is showing huge goodwill and intangible asset in it books after its merger with Glaxo division ?? Will this have impact on its book value

1. When a company acquired another company, the money paid in excess of book value of the acquired company is recorded in the balance sheet as “intangible equity”.

Very normal and nothing suspicious about it, unless your estimate is that the company paid much higher price that the true value of the company that has been acquired.

2. Book value does not have too much relevance in the case of HUL

It does a lot of contract manufacturing and basically its a marketing machine. So, it does not require large factories and machinery and other fixed assets